Structured Settlement vs. Lump Sum: Which Settlement Payout Is Right for You?

Reaching a settlement after an accident or lawsuit is a huge emotional relief. But once the case is finally over, you face one last, critical question:

“Do you want all your settlement money now, or do you want it paid out over time?”

In most cases, that choice comes down to two paths:

- A lump sum – one large payment that lands in your bank account.

- A structured settlement – a series of tax-advantaged, scheduled payments funded by an annuity.

There is no one-size-fits-all answer. The “best” option isn’t just about how big your settlement is. It depends on your age, your financial habits, whether you rely on government benefits, and how comfortable you are managing money and investment risk.

This guide will walk you through how each payout choice works, the pros and cons of a structured settlement vs lump sum, and real-world scenarios to help you decide which settlement payout is right for you.

If you’re also deciding how to protect a child’s settlement, you may want to read:

- Blocked Account vs. Structured Settlement for Minors

- Can Parents Sell a Minor’s Structured Settlement?

- How Structured Settlement Payments Actually Work

1. The Two Paths of Financial Recovery

Think of your settlement decision as a fork in the road:

- Lump Sum – You take your net settlement money all at once.

- Structured Settlement – You arrange for guaranteed payments over time using a structured settlement annuity.

On the surface, taking a lump sum looks like “freedom” and a structured settlement looks like “restriction.” But when you look at taxes, long-term security, and the risk of mismanaging a large check, the comparison becomes more nuanced.

Your attorney or settlement planner may show you different illustrations. This article will help you understand what those numbers really mean, in plain English.

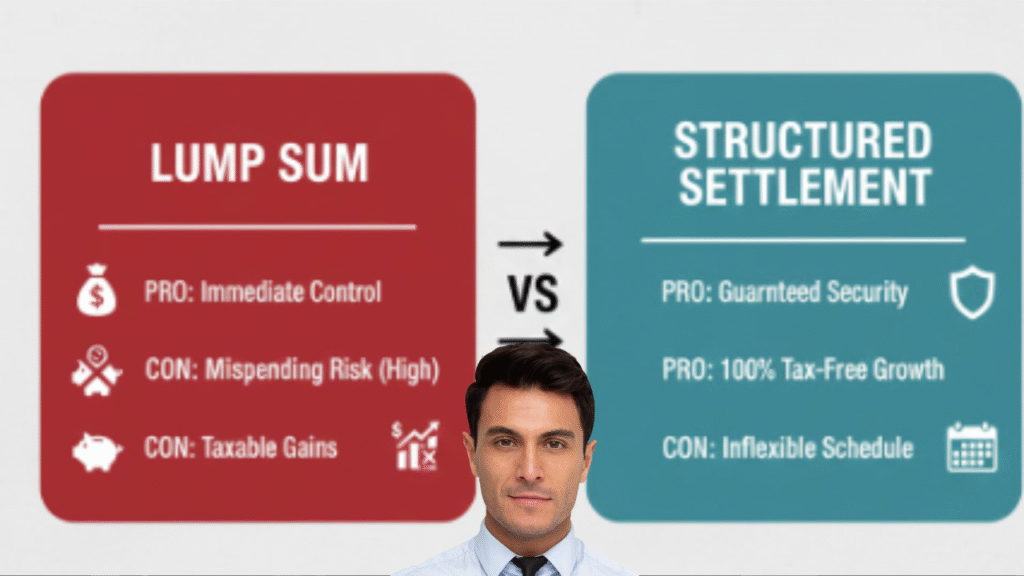

2. Option A: Lump Sum Settlement – Freedom and Risk

2.1 What Is a Lump Sum Settlement?

A lump sum settlement means you receive your net settlement—after attorney fees, case costs, and medical liens—in one single payment. The check is written to you (and sometimes your attorney), and once it clears, the money is yours to manage.

People often picture this as a life-changing windfall. In reality, a lump sum can be an incredible opportunity or a serious trap, depending on how it’s handled.

2.2 Advantages of Taking a Lump Sum

- Immediate control: You decide where every dollar goes from day one.

- Debt payoff: You can pay off high-interest credit cards, medical bills, or a mortgage quickly.

- Investment potential: If you are financially savvy, you may invest in stocks, bonds, real estate, or a business with returns higher than any annuity.

- Flexibility for big goals: Starting a business, buying a home, or relocating may be easier with a large cash base.

For a disciplined investor with a solid financial plan, a lump sum can be a powerful tool.

2.3 The Hidden Downsides of a Lump Sum

Unfortunately, many people underestimate the risks that come with total control.

1. The “Lottery Curse” and Misspending Risk

Studies on lottery winners and large cash recipients repeatedly show a sobering pattern: a large percentage end up broke or deeply stressed within just a few years. The same danger can apply to a big settlement check.

Common lump sum settlement bad ideas include:

- Buying a brand-new luxury car or truck that rapidly loses value.

- Investing heavily in a friend’s unproven business venture.

- Day trading or speculative crypto investing without experience.

- Overspending on lifestyle upgrades: vacations, gadgets, and gifts.

When the money runs out, the medical issues or reduced earning capacity from your injury may still be there, but your safety net is gone.

2. Investment and Market Risk

If you choose a lump sum, your financial future depends heavily on investment choices. Markets can be volatile. A bad year (or a bad advisor) can erase years of potential security. Gains from investing a lump sum are also taxable, unlike many structured settlement payments.

3. Emotional and Family Pressure

Large checks attract attention. You may face pressure from relatives, friends, or salespeople pushing investments, “opportunities,” or urgent requests for help. It is very hard to say no when you are the only person in the room with money.

3. Option B: Structured Settlement – Security and Discipline

3.1 What Is a Structured Settlement?

A structured settlement uses part or all of your settlement to buy an annuity from a highly-rated life insurance company. That annuity then pays you over time, following a schedule you agree on while the case is still being resolved.

For example, you might arrange for:

- $2,000 per month for 20 years

- Plus $25,000 at age 30 and $50,000 at age 40

If you’d like a deeper explanation of the mechanics, including who actually pays you and how the money moves from the court to your bank, see: How Structured Settlement Payments Actually Work .

3.2 Tax Advantages: The Biggest Hidden Benefit

In many physical injury and physical sickness cases, structured settlement payments are income tax-free under Internal Revenue Code Section 104(a)(2) .

That means:

- The principal portion of your settlement is tax-free.

- The interest and growth inside the annuity are also tax-free.

By contrast, if you take a lump sum and invest it yourself, the investment income is generally taxable. Over many years, that tax advantage can make a structured settlement surprisingly competitive with traditional investments—without the same level of risk.

3.3 Pros of a Structured Settlement

- Built-in discipline: You can’t accidentally spend all your money in one year.

- Predictable, guaranteed payments: The annuity issuer is contractually obligated to pay on schedule.

- Reduced emotional pressure: There’s no giant visible bank balance for others to target.

- Long-term planning: You can match payments to life milestones (education, housing, retirement).

- Protection from market crashes: Your payments are not directly tied to daily stock market swings.

3.4 Cons of a Structured Settlement

- Inflexible schedule: Once the structure is set and court-approved, it’s very hard to change.

- Limited access to cash: You cannot simply “withdraw extra” the way you would from a savings account.

- No big upfront windfall: If you have urgent large expenses, a pure structure may feel too restrictive.

- Potential inflation drag: Many structures have fixed payments that may not fully keep up with inflation.

For a claimant who wants stability and doesn’t want to constantly manage money, these tradeoffs are often worth it.

4. Structured Settlement vs. Lump Sum: Head-to-Head Comparison

Here is a side-by-side comparison that highlights the core differences between a lump sum award and a structured settlement.

| Feature | Lump Sum | Structured Settlement |

|---|---|---|

| Tax Status | Principal is often tax-free; investment earnings are taxable. |

For qualifying physical injury cases, principal and growth are tax-free. |

| Security | Depends on your investment decisions and market conditions. | Payments guaranteed by the issuing life insurance company, subject to its claims-paying ability. |

| Control | Full, immediate control over the entire amount. | Payments follow a fixed schedule; limited ability to change later. |

| Inflation Risk | Can be mitigated with smart investing; also can be worsened by poor choices. | Fixed payments may lose purchasing power if inflation rises faster than expected. |

| Misspending Risk | High – easy to overspend early. | Low – built-in “speed limit” on spending. |

| Best For | Financially savvy, disciplined individuals or those needing large immediate funds. | Claimants seeking long-term security, minors, and those wary of managing large sums. |

For more detail on how structures are used for children, including the tradeoffs with blocked bank accounts, see: Blocked Account vs. Structured Settlement for Minors .

5. Decision Framework: Which Settlement Payout Is Right for You?

Instead of asking, “Is a structured settlement better than a lump sum?” a more useful question is: “Which option fits my actual life, personality, and needs?”

Scenario 1: Young Claimant With Little Financial Experience

Age: 18–30. Little or no experience managing large sums. Maybe already dealing with medical issues or interrupted education.

Risks: Peer pressure, impulsive spending, lack of budgeting, and no investing background.

Verdict: A structured settlement (possibly combined with a modest lump sum) often makes the most sense. It creates a steady, reliable stream of income and protects your future self from your current inexperience.

Scenario 2: Financially Savvy Adult or Professional Investor

Age: 35–60. Comfortable with budgeting and investing, possibly already working with a fiduciary financial planner.

Opportunity: You may be able to invest a lump sum in a diversified portfolio and, over time, earn higher returns than a conservative annuity, even after taxes.

Verdict: A lump sum or a hybrid (part lump sum, part structured) can be a good fit—provided you commit to a serious, long-term financial plan.

Scenario 3: Claimant With Ongoing Medical or Living Needs

Some claimants rely on regular funds to cover medications, therapies, or reduced ability to work. Here, consistency matters more than chasing high returns.

Verdict: A structured settlement tailored around your monthly budget, health expenses, and expected lifespan can reduce stress and provide crucial stability.

Scenario 4: Claimant Relying on Medicaid or SSI

If you receive needs-based benefits like Supplemental Security Income (SSI) or Medicaid, suddenly holding a large lump sum in your name can push you over asset limits and cause you to lose benefits.

In these situations, a combination of a structured settlement and a properly drafted Special Needs Trust may be critical. This is a complex area—be sure to work with an attorney experienced in public benefits and settlement planning.

Scenario 5: You Need Cash Now but Also Want Long-Term Protection

Many people fall in the middle. They have urgent needs—paying off a mortgage, buying a reliable car, or catching up on bills—but they also worry about burning through everything too quickly.

Verdict: A hybrid structure (sometimes called a partial structured settlement) can balance both goals: you take some money in a lump sum and place the rest into a structured settlement for long-term income.

6. Common “What If” Fears and How to Think About Them

What If the Insurance Company Goes Bankrupt?

Structured settlement annuities are issued by life insurance companies that are heavily regulated and monitored. You can review their financial strength ratings through agencies such as A.M. Best or on platforms like Yahoo Finance.

In the rare event an insurer fails, most states have a life and health insurance guaranty association that provides a safety net up to certain limits. These limits vary by state. You can learn more from the National Organization of Life & Health Insurance Guaranty Associations.

This doesn’t mean there is zero risk, but it does mean structured settlement payments are not simply “lost” if an insurer gets into trouble. Regulators typically work to transfer policies to a stronger carrier or provide partial coverage under state law.

What If I Need Cash Later and Chose a Structured Settlement?

Once your structure is in place, you generally cannot call the insurer and change the payment schedule. The main way people get cash earlier is by selling some of their future payments to a factoring company.

Be careful here. Selling payments:

- Usually requires court approval under structured settlement protection acts.

- Involves a discount rate that can significantly reduce the total value you receive.

- Should be evaluated with an attorney or independent advisor, not just a sales rep.

In short, selling can provide short-term relief, but at a high long-term cost.

7. FAQs: Real Questions People Ask About Structured Settlements vs. Lump Sums

1. What is the difference between a lump sum and a structured settlement?

With a lump sum, you receive your net settlement in one payment and must manage it yourself. With a structured settlement, your settlement funds are used to buy an annuity that pays you over time. The structured approach emphasizes long-term security and, in many cases, tax-free payments.

2. Are structured settlement payments really tax-free?

For many physical injury and physical sickness cases, yes. Under IRC §104(a)(2), these payments are typically excluded from gross income. But not every type of damage is treated the same way, so always confirm with your tax professional.

3. Can I take part lump sum and part structured settlement?

Yes, and this is often the most practical solution. You might take enough cash upfront to pay debts and handle urgent needs, and structure the rest for steady future income. Many experienced settlement planners favor this blended strategy.

4. Are attorney fees taken out before I choose lump sum vs structure?

In general, attorney fees and case costs are deducted from the gross settlement amount first. The remaining net settlement is what you decide to take as a lump sum, a structure, or a combination of both. Your attorney should clearly explain this accounting to you.

5. Is it safe to invest a lump sum on my own?

It can be, but it depends on your plan and your behavior. Working with a fiduciary financial advisor who must put your interests first is a good starting point. Be cautious of high-pressure sales pitches, complex products you don’t understand, or “guaranteed” returns that sound too good to be true.

6. Can I change my structured settlement later if my life situation changes?

Structured settlements are intentionally designed to be difficult to change. In most cases, you cannot simply modify the payment dates or amounts. Court-approved sales of payment rights are sometimes allowed, but they usually come with a steep financial discount.

7. Which is better for minors: lump sum or structured settlement?

Courts are often very cautious about minors receiving large lump sums. For children, judges frequently favor structured settlements or court-blocked accounts. To understand this better, see: Blocked Account vs. Structured Settlement for Minors .

8. Does a structured settlement affect my credit score?

No. Merely having a structured settlement does not show up as a loan or liability on your credit report. However, how you manage your overall finances—credit cards, loans, and bills—will still affect your score.

9. What if inflation gets very high?

If inflation rises sharply, fixed structured settlement payments may lose purchasing power over time. You can partly address this by designing payments that increase at set percentages, or by combining a structure with some lump-sum funds invested in assets that historically outpace inflation. For a general explanation of inflation risk, see Investopedia’s guide to inflation risk.

10. Who can help me decide between a structured settlement and a lump sum?

You don’t have to make this decision alone. It’s smart to talk with:

- Your trial attorney

- A certified structured settlement consultant

- A fiduciary financial planner

- A tax advisor who understands personal injury settlements

Each professional sees a different angle—legal, financial, and tax—and together they can help you choose a payout structure that matches your real life, not just a spreadsheet.

8. Conclusion: Peace of Mind vs. Potential Riches

At the end of the day, choosing between a structured settlement vs a lump sum is really choosing between two different kinds of peace of mind.

- A lump sum offers the peace of mind of full control and immediate access—but demands discipline and financial skill.

- A structured settlement offers the peace of mind of guaranteed income and tax advantages—but requires you to accept less flexibility.

For many people, the right answer is not “all or nothing” but a carefully designed combination. Before you sign anything, ask your attorney or settlement planner to show you both options side-by-side, with realistic assumptions and clear explanations.

Taking a little extra time now to understand your choices can make the difference between a settlement that quietly supports your life for decades—and one that disappears much faster than you ever imagined.

Disclaimer: This article is for general educational purposes only and does not constitute legal, tax, or financial advice. Always consult qualified professionals about your specific situation.

1 thought on “Structured Settlement vs. Lump Sum: Which Settlement Payout Is Right for You?”