Structured Settlement Protection Acts (SSPA): How Courts Regulate the Sale of Structured Settlement Payments

Structured Settlement Protection Acts (SSPAs) are state laws that control how a person can transfer (sell) the right to receive future structured settlement payments. The central idea is simple: if you are giving up guaranteed future income for cash today, the deal should be reviewed by a court to reduce the risk of pressure, confusion, or unfair pricing.

This guide explains what the law requires, how judges evaluate petitions, and what changes from state to state. It also includes a practical state-by-state checklist table you can use to prepare for a court hearing—especially if your settlement involves a minor or dependents.

- Overview: what an SSPA regulates

- Why SSPAs exist

- Core legal requirements (common across states)

- How the court-approval process works

- Expert commentary (Rajiv Sethi)

- Special rules and scrutiny when minors are involved

- Federal law overlay: why “court approval” is non-negotiable

- State-by-state requirements (quick reference)

- Practical preparation checklist

- Frequently asked questions

Overview: What an SSPA Regulates

A structured settlement is a legal compensation arrangement—most commonly for personal injury, medical malpractice, or wrongful death—where funds are paid over time rather than in a single lump sum. Payments are typically funded through an annuity issued by a life insurance company and backed by the obligor’s settlement terms.

When a payee wants to sell some or all of those future payments to a factoring company in exchange for a lump sum, an SSPA usually treats that transfer as a regulated transaction requiring a court order. In plain terms: the deal is not “final” just because the payee signs a contract.

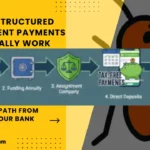

If you want a plain-English walkthrough of how payments flow from settlement documents to actual deposits, see: how structured settlement payments actually work (the 5-step path from court to your bank account) .

SSPAs do not automatically ban sales. They require transparency, notice, and a judge’s “best interest” review before payments can be redirected. [Citation Placeholder A1]

Why Structured Settlement Protection Acts Exist

SSPAs were adopted nationwide because structured settlement recipients often face real-world pressure: medical bills, disability, life disruptions, and urgent family needs. In that environment, it is easy to underestimate how much long-term income you are giving up when you accept a discounted cash offer.

The secondary market can be legitimate—but it can also incentivize aggressive sales tactics and pricing that is difficult for a non-expert to evaluate. SSPAs exist to force a “pause” in the process so the economics are explained, the math is visible, and the court can intervene if the transaction looks harmful. [Citation Placeholder A2]

If you are weighing the bigger decision—income over time versus cash today—start here: Structured Settlement vs. Lump Sum Settlement. Many court questions in SSPA hearings are essentially a more formal version of that comparison.

Core Legal Requirements (Common Across States)

While wording varies, most SSPAs share the same backbone. Courts typically look for the following pillars:

1) Mandatory Court Approval

A transfer generally cannot be enforced unless a court approves it. The court order is the “gate” that allows the annuity issuer/obligor to redirect payments. [Citation Placeholder A3]

2) A “Best Interest” Finding

Judges commonly must find that the transfer is in the payee’s best interest—and in many states, also the best interest of the payee’s dependents. Even if a seller wants the cash, a judge can deny the petition if the tradeoff looks unreasonable.

3) Required Disclosures (Clear Economics)

SSPA disclosures typically include:

- Which payments are being sold (amounts and due dates)

- The total of those payments (gross future value)

- A present value calculation (discounted present value)

- The net amount the seller will receive

- Fees/costs and who pays them

- An effective discount rate (or equivalent economic cost measure)

This is one reason “small” fee differences matter: fees plus discount rate can materially change the net proceeds. [Citation Placeholder A4]

4) Notice to Interested Parties

SSPAs commonly require notice to entities such as the annuity issuer, the obligor, and sometimes beneficiaries or other parties named in the settlement documents. The goal is to give any affected party a chance to respond.

5) Cooling-Off / Cancellation Rights (in many states)

Some states provide an explicit cancellation period, or impose waiting periods or procedural timing rules that effectively create a cooling-off window. [Citation Placeholder A5]

How the Court-Approval Process Works

The process varies by jurisdiction, but the structure is broadly consistent:

- Transfer agreement signed (subject to court approval)

- Petition filed in the proper court (often tied to residence or original settlement venue)

- Disclosures served and supporting documents attached (payment schedules, present value, fee breakdown)

- Interested parties notified (issuer/obligor and others as required)

- Hearing held (often with payee appearance; sometimes remote with permission)

- Judge issues order approving or denying

For readers new to the concept of selling payments, you may also want: the 5-step payment path guide , and—if the payee is a minor: can parents sell a minor’s structured settlement?

Expert Commentary: What Judges Actually Focus On

Practical takeaway: Your paperwork should read like a clear business case—what is being sold, why it is necessary, and why the economics are fair. [Citation Placeholder EXP-1]

SSPAs and Minors: Heightened Scrutiny and Alternatives

When a settlement involves a minor, courts typically apply stricter scrutiny because minors cannot legally consent in the same way adults can, and settlement funds are often meant to support long-term medical care, education, and stability.

If your case involves a child, these guides will help you understand the framework courts are protecting:

- Structured settlements for minors: a complete guide

- Blocked account vs. structured settlement for minors

- Can parents sell a minor’s structured settlement?

In many minor-related cases, courts prefer protective structures (for example, restricted/blocked accounts or structured payout schedules) rather than permitting a transfer that reduces the child’s future security. [Citation Placeholder MIN-1]

Federal Law Overlay: Why “Court Approval” Is Non-Negotiable

Although SSPAs are state laws, federal tax rules strongly reinforce the court-approval requirement for structured settlement factoring transactions. The most cited provision is 26 U.S.C. § 5891, which imposes a substantial excise tax on certain non-qualified transfers.

External authority links (non-competitor):

- Legal Information Institute (Cornell Law School): 26 U.S.C. § 5891 — Structured settlement factoring transactions [External Authority]

- NCOIL model reference (legislative model used by many states): National Council of Insurance Legislators (NCOIL) [External Authority]

- IRS general tax topic entry point (for background and definitions): Internal Revenue Service (IRS) [External Authority]

If a factoring transaction attempts to bypass court approval, it can trigger severe consequences for the purchaser under federal tax rules, which is one reason reputable transfers are structured to comply with both state SSPA procedures and federal requirements. [Citation Placeholder FED-1]

State-by-State SSPA Requirements (Quick Reference)

Every state (and D.C.) has an SSPA, but the “extras” differ: some require independent professional advice, some restrict transfers tied to workers’ compensation, some impose special filing rules (county of residence), and others require additional disclosures or agency filings.

Important: This table is a practical checklist summary, not legal advice. Always confirm the current statute and local court rules for your jurisdiction. [Citation Placeholder ST-0]

| Jurisdiction | Common “extra” requirement(s) you should plan for |

|---|---|

| Alabama | Detailed disclosures are emphasized; expect the court to focus on clarity of terms and economics. [ST-AL] |

| Alaska | Written disclosure of key terms; courts may strongly encourage independent advice. [ST-AK] |

| Arizona | Buyer typically must advise payee in writing to seek independent professional advice. [ST-AZ] |

| Arkansas | Some restrictions can limit splitting/assigning certain payment structures; confirm allowed transfer scope. [ST-AR] |

| California | Enhanced consumer-protection posture; expect robust notice/document standards; additional filings may be required in some contexts. [ST-CA] |

| Colorado | Written recommendation to seek independent advice is common; some claims (e.g., certain comp-related streams) may face restrictions. [ST-CO] |

| Connecticut | Written advice recommendation is typical; court examines understanding and voluntariness closely. [ST-CT] |

| Delaware | Independent professional advice is often expected; notice to beneficiaries may be required. [ST-DE] |

| District of Columbia | Additional disclosure history may be relevant (prior attempted/denied transfers). [ST-DC] |

| Florida | Petitions often tied to county of residence; independent advice is frequently required; procedural updates exist in recent years. [ST-FL] |

| Georgia | Cancellation windows can be longer than many expect; confirm timing rules before filing. [ST-GA] |

| Hawaii | Core disclosures are central; judges often focus on whether the payee understands the discount and fee impact. [ST-HI] |

| Idaho | Written recommendation for independent advice is common; some benefit streams may be restricted. [ST-ID] |

| Illinois | Economic disclosures (including effective rate concepts) and payee participation at hearing may be emphasized. [ST-IL] |

| Indiana | Some workers’ compensation-related transfers can be restricted; confirm claim type and assignability. [ST-IN] |

| Iowa | Strict disclosure formatting/timing may apply; courts expect precise numbers and itemized costs. [ST-IA] |

| Kansas | Some comp-related transfers restricted; standard best-interest review remains core. [ST-KS] |

| Kentucky | Disclosure is central; some benefit streams restricted; beneficiary notice can matter. [ST-KY] |

| Louisiana | Independent advice can be important; font-size/format rules may apply to disclosures in some cases. [ST-LA] |

| Maine | Independent advice often expected; settlement documents may require additional consents if anti-assignment clauses exist. [ST-ME] |

| Maryland | Registration/oversight features may apply; heightened scrutiny if cognitive impairment factors are present. [ST-MD] |

| Massachusetts | Independent professional advice is frequently a focus; judges probe understanding of long-term impact. [ST-MA] |

| Michigan | Some caps/constraints can apply (rates/fees in certain contexts); comp-related transfers may be restricted. [ST-MI] |

| Minnesota | Independent advice often required; additional safeguards may be used for payees with possible impairments. [ST-MN] |

| Mississippi | Written advice recommendation is typical; court focuses on fairness and disclosure completeness. [ST-MS] |

| Missouri | Fair-value language may be prominent; some streams (e.g., comp) can be restricted. [ST-MO] |

| Montana | Comp-related restrictions may exist; confirm whether the underlying settlement stream is transferable. [ST-MT] |

| Nebraska | Advice notices and interest-rate limits can apply; comp-related restrictions may exist. [ST-NE] |

| Nevada | Itemized expenses disclosures may be scrutinized; written advice recommendation common. [ST-NV] |

| New Hampshire | Later-adopting state; confirm specific statutory release/liability language and petition requirements. [ST-NH] |

| New Jersey | Advice notices are common; venue/procedure rules can be particular. [ST-NJ] |

| New Mexico | Disclosure timing requirements may apply; courts often focus on whether disclosures were served early enough. [ST-NM] |

| New York | Procedural formality can be strict; documentation/notice methods may be constrained; expect close scrutiny. [ST-NY] |

| North Carolina | Rate/fee limits may apply; independent advice may be required; comp-related restrictions may exist. [ST-NC] |

| North Dakota | Hardship findings may be treated differently than other states; confirm statutory test. [ST-ND] |

| Ohio | Independent advice often required; comp-related restrictions may exist; detailed disclosures expected. [ST-OH] |

| Oklahoma | Written advice recommendation typical; courts focus on informed consent and deal economics. [ST-OK] |

| Oregon | Standard court approval + best-interest review; confirm any local court procedural preferences. [ST-OR] |

| Pennsylvania | Advice recommendation or written waiver may be relevant; confirm local filing and hearing practices. [ST-PA] |

| Rhode Island | Written advice recommendation typical; disclosure completeness is central. [ST-RI] |

| South Carolina | Advice recommendation typical; comp-related restrictions may exist. [ST-SC] |

| South Dakota | Advice recommendation typical; expect best-interest review to drive outcomes. [ST-SD] |

| Tennessee | Advice recommendation typical; comp-related restrictions may exist. [ST-TN] |

| Texas | Advice recommendation typical; venue and notice compliance matters; disclosure math is heavily reviewed. [ST-TX] |

| Utah | Advice recommendation typical; confirm court location and document requirements. [ST-UT] |

| Vermont | Court may require detailed findings on purpose/need and fairness; expect thorough questioning. [ST-VT] |

| Virginia | County-of-residence filing may apply; prior transfer history can matter; procedural updates exist. [ST-VA] |

| Washington | Advice recommendation typical; courts focus on disclosures and best-interest test. [ST-WA] |

| West Virginia | Extra waiting time can apply in some scenarios; confirm timeline and hearing scheduling. [ST-WV] |

| Wisconsin | Disclosure model-based approach; payee appearance rules may apply; effective rate concepts can be emphasized. [ST-WI] |

| Wyoming | Strong disclosure detail expectations (amounts, dates, gross advance, itemized fees). [ST-WY] |

We are building state-by-state guides that translate your local SSPA into a practical checklist (venue, disclosures, hearing expectations, and common denial reasons). When those pages go live, this section will link to your state’s guide. [Citation Placeholder ST-HUB]

In the meantime, if your situation involves a minor, start here: Blocked Account vs Structured Settlement for Minors.

Practical Preparation Checklist (What Courts Expect to See)

If you want to improve approval odds (and reduce delays), prepare your petition package as if you were explaining the transaction to a skeptical reader: clear numbers, clear reasons, and no missing pieces.

Deal economics: make the math easy to verify

- Attach a payment schedule (amounts + due dates) and clearly mark the payments being sold.

- Provide present value math and define assumptions (discount rate approach, timing conventions). [Citation Placeholder PR-1]

- Itemize every fee and show net-to-payee amount.

Best-interest narrative: explain “why now”

- State the purpose (medical need, housing stability, education, debt restructuring, etc.).

- Explain why alternatives are not sufficient (budget plan, partial sale vs full sale, refinancing, etc.).

- If dependents rely on payments, address how their needs remain protected.

Process compliance: avoid procedural denials

- Confirm correct venue (often tied to residence or settlement jurisdiction). [Citation Placeholder PR-2]

- Confirm notice requirements (issuer/obligor and any additional required parties).

- Confirm whether independent professional advice is required or must be waived in writing.

- Confirm any cooling-off or waiting-period rules.

If you are deciding whether selling makes sense at all, revisit: Structured Settlement vs Lump Sum Settlement. Many denials occur when the “why” is unclear or when the long-term harm outweighs the short-term benefit.

Frequently Asked Questions

What is a Structured Settlement Protection Act (SSPA)?

An SSPA is a state law that governs transfers of structured settlement payment rights and typically requires court approval before payments can be redirected. [Citation Placeholder FAQ-1]

Do all states have SSPAs?

Yes. Every U.S. state and the District of Columbia has enacted an SSPA framework. [Citation Placeholder FAQ-2]

Can a payee sell only part of the payments?

Often yes, but the court will still evaluate the economics and best-interest impact. Some states have practical or statutory constraints that make certain splits harder. [Citation Placeholder FAQ-3]

Can parents sell a minor’s structured settlement?

Parents/guardians cannot simply “approve” a sale on their own. Courts apply heightened scrutiny to protect the child’s interests. Read more: Can parents sell a minor’s structured settlement?

What do judges usually ask in a hearing?

Judges typically test whether you understand the transfer, the discount/fees, the long-term impact, and whether the stated purpose is legitimate and necessary. The court may also focus on dependents and alternatives. [Citation Placeholder FAQ-4]

Key Takeaways

- SSPAs require court approval to help prevent unfair or confusing transfers of payment rights.

- Disclosures matter: present value, fees, and net proceeds must be easy to verify.

- Judges apply a best-interest standard and can deny even “agreed” deals.

- Minors receive stronger protection and courts often prefer conservative alternatives.

- State rules vary—venue, advice requirements, waiting periods, and special restrictions differ.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Laws and procedures vary by jurisdiction. Consult qualified professionals for guidance on your specific situation.