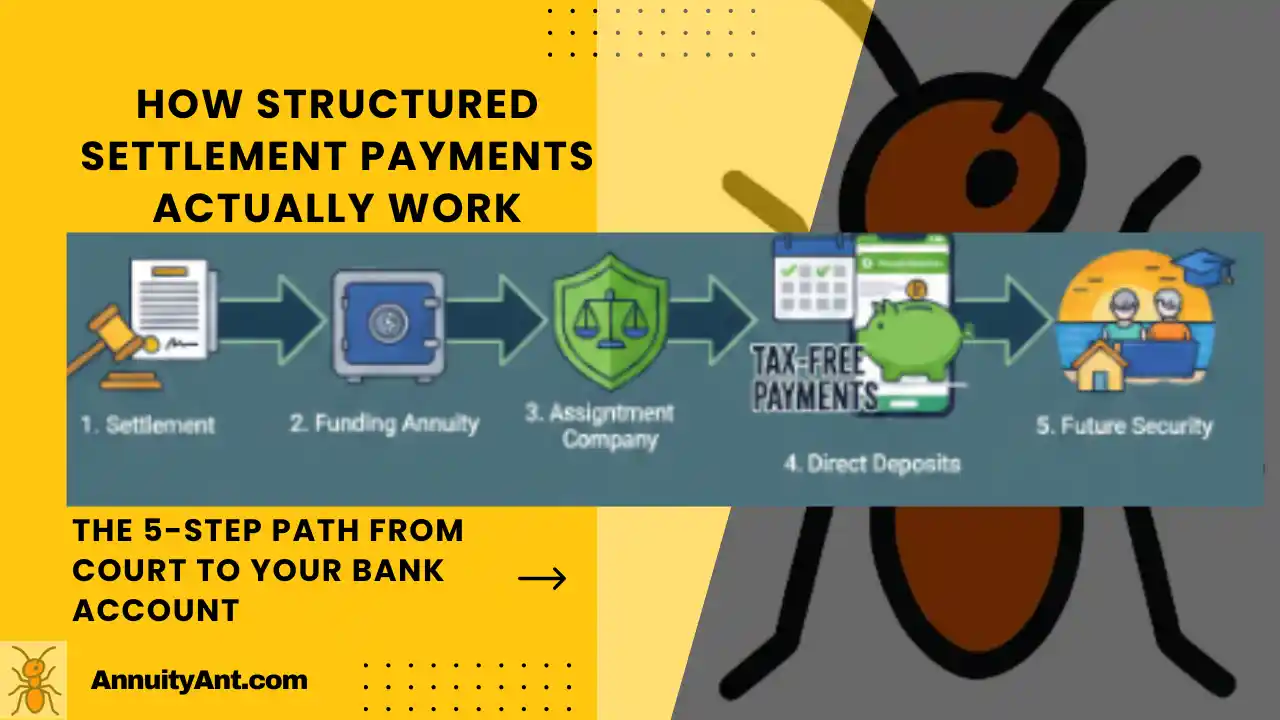

How Structured Settlement Payments Actually Work: The 5-Step Path from Court to Your Bank Account

Primary keyword: how do structured settlement payments work

You may have been told, “You’ll receive structured settlement payments for years,” but nobody really explained how the money actually gets from the defendant to your bank account.

This guide breaks the process into a simple, five-step path—from the court order, to the insurance company, to your monthly or annual payments. We will also cover:

- Who pays your structured settlement annuity

- The timeline for structured settlement payments

- What happens if the structured settlement company goes bankrupt

This is an educational overview, not legal or tax advice. For personal guidance, speak with an attorney, tax advisor, or settlement planner.

If your case involved a child, you may also want to read:

- Blocked Account vs Structured Settlement for Minors

- Can Parents Sell a Minor’s Structured Settlement?

Step 1: The Settlement Agreement – Your Financial Blueprint

The structured settlement story begins with a legal document called the settlement agreement, sometimes combined with a “release” or “stipulation for settlement.” This is the blueprint for how your future payments will work.

What the Settlement Agreement Really Does

The agreement:

- States the total value of the settlement

- Defines how and when you will be paid (monthly, yearly, lump sums at specific ages, or a mix)

- Authorizes using a structured settlement annuity to fund the payments

Important clarification: the defendant or their insurer does not send you checks every month. Their main role is to fund the annuity that will ultimately pay you.

Example of a Simple Structured Payment Schedule

A settlement agreement might say something like:

- $1,000 per month for 20 years, starting on June 1, 2026

- Plus lump-sum payments of $25,000 at ages 30 and 35

Those dates and amounts become the instructions for the next step: purchasing the annuity.

Step 2: Funding the Structured Settlement Annuity

Once the court approves the settlement, the defendant or their insurance company does not keep an ongoing payment obligation. Instead, they pay a lump sum to a company that will fund your future payments.

How the Annuity Purchase Works

- The defendant or liability insurer agrees to pay a certain amount to resolve your claim.

- Instead of paying you all the money in cash, they use part or all of it to buy an annuity from a life insurance company that specializes in structured settlements.

- The price they pay for the annuity is based on current interest rates and the exact schedule of payments in your settlement agreement.

This annuity is known as a structured settlement annuity. It is a contract with a highly rated life insurer whose job is to make your future payments, exactly as promised.

From this point on, the life insurance company (and its affiliates) are at the center of “how structured settlement payments work”—not the defendant.

Step 3: The Assignment Company – Who Actually Owes You Money?

This part confuses many people. Your settlement documents may mention an “Assignment Company” or “Qualified Assignment Company.” This company often has a similar name to the life insurer that issued the annuity.

What the Assignment Company Does

In simple terms, the assignment company:

- Takes over the obligation to make your structured settlement payments

- Enters into a separate contract to receive the annuity payments from the life insurer

- Promises to pass those payments on to you, exactly as scheduled

Legally, this is called a “qualified assignment”. It is allowed under U.S. tax law so that your payments remain tax-advantaged and the defendant is fully released from the long-term obligation.

Why This Protects You

The assignment setup helps protect you if:

- The original defendant goes bankrupt

- The company you sued merges, is sold, or shuts down

Your right to receive the payments is now tied to the life insurance company and the assignment company, not to the business that injured you. That’s a key reason structured settlements are considered safer than simple promises to pay.

Step 4: Payment Mechanics & the Tax-Free Pipeline

At this point, the annuity has been purchased and the assignment company has taken on the payment obligation. Now we get to what most people really care about:

“How do structured settlement payments actually show up in my bank account?”

How the Money Moves Each Month or Year

- The life insurance company sends payments to the assignment company according to the annuity contract.

- The assignment company then directs those payments to you on the agreed schedule.

- You receive the funds by:

- Direct deposit (most common and secure), or

- Paper check mailed to your address on file

If you change banks or move to a new address, you must notify the insurance company or its administrator and fill out their change forms. It’s wise to keep copies of:

- Your original settlement agreement

- Any welcome letters or certificates from the life insurer

- Customer service phone numbers and policy/contract numbers

Why Structured Settlement Payments Are Usually Tax-Free

For many physical injury or sickness cases, your structured settlement payments are income tax-free under Internal Revenue Code Section 104(a)(2). This is a major advantage over regular investment income.

In plain language, that means:

- You don’t pay federal income tax on the structured settlement payments themselves

- You don’t pay tax on the interest or growth generated inside the annuity

Always confirm your specific tax situation with a qualified tax professional, especially if your case is not a standard physical injury claim (for example, employment or punitive damages).

Step 5: Timeline – When Do Structured Settlement Payments Start?

Another common question is: “How long before I see my first structured settlement payment?”

The exact timing varies by case and insurer, but here is a typical timeline for structured settlement payments once everything is approved:

Typical Timeline

- Week 1–2: Court approves the settlement; paperwork is finalized.

- Week 2–4: Defendant/insurer pays the lump sum to the assignment company and/or directly to the life insurer.

- Week 4–8: Annuity is issued; policy number is created; payment instructions are set up.

- Month 2–3: First payment is made on the date specified in your settlement agreement.

Important: Your first payment date should be clearly listed in your settlement paperwork. If that date passes and you haven’t been paid, contact the insurer or administrator immediately.

Once the system is up and running, payments generally continue like clockwork—monthly, annually, or on whatever schedule you chose.

What Happens If the Structured Settlement Company Goes Bankrupt?

This is one of the most worrying questions for recipients and a high-value topic to understand: what happens if the structured settlement company goes bankrupt?

There are two main entities people worry about:

- The life insurance company that issued the annuity

- The assignment company that formally owes you the payments

If the Life Insurance Company Fails

Life insurance companies are heavily regulated at the state level. In the rare event that a life insurer becomes insolvent, most states have a Life & Health Insurance Guaranty Association that provides a safety net up to certain limits (often in the range of $250,000–$500,000 per person, though this varies by state).

In a failure scenario, regulators typically try to:

- Transfer annuity obligations to another solvent insurer, or

- Use guaranty association coverage to keep payments going, up to legal limits

The outcome depends on the specific state and the details of your contract, but the key point is: you are not simply left with nothing.

If the Assignment Company Fails

Assignment companies are usually thin entities created specifically to hold structured settlement obligations. If an assignment company goes out of business, its obligations are typically transferred to another entity in the same corporate family or to a successor company. Because the underlying annuity is still in place, your payments generally continue.

If you ever receive notice about a merger, acquisition, or transfer of servicing, keep those letters together with your original settlement documents.

For detailed reassurance about your specific insurer, you can:

- Look up its financial strength rating (A, A+, etc.) with major rating agencies

- Contact your state’s insurance department or guaranty association

Who Pays My Structured Settlement, in Plain English?

Let’s simplify the entire process into three sentences:

- The defendant or its insurer pays a lump sum to fund your structured settlement annuity.

- The assignment company takes over the legal obligation to make your future payments.

- The life insurance company uses the annuity to send money on schedule, which arrives in your bank account or mailbox.

That’s the real answer to the question: “Who pays my structured settlement annuity?”

Can You Change Your Payment Schedule Later?

One of the trade-offs with structured settlements is that they are designed to be permanent. Once the schedule is locked in and the annuity is purchased, you generally cannot call the insurer and ask to:

- Speed up payments

- Pause payments

- Switch monthly payments to a lump sum

The main way people change their schedule is by selling some or all of their future payments to a factoring company for a discounted lump sum. This is a complex, heavily regulated process and usually requires court approval. It can also be very expensive, which is why it deserves a separate, careful discussion.

If you are considering selling payments from a child’s settlement, make sure to read: Can Parents Sell a Minor’s Structured Settlement?

Visual Overview: From Court Order to Your Bank Account

Create a simple flow diagram with these boxes and arrows:

Court Approves Settlement → Defendant/Insurer Funds Annuity → Assignment Company Takes Obligation → Life Insurance Company Issues Payments → Money Deposited to You

This visual makes it easy for readers (and Google) to understand how structured settlement payments work step-by-step.

Structured Settlement Payments FAQ

1. How do structured settlement payments actually work?

Your settlement agreement sets a payment schedule. The defendant or their insurer then funds a structured settlement annuity from a life insurance company. An assignment company takes over the obligation and sends you payments (by check or direct deposit) on the agreed dates—often for many years or even life.

2. Who pays my structured settlement annuity?

Initially, the defendant or their insurer funds the annuity. After that, the assignment company and the life insurance company work together to send your payments. The original defendant normally has no ongoing payment role once the structure is in place.

3. How long does it take to get my first structured settlement payment?

In many cases, the first payment arrives within 1–3 months after the court approves the settlement and all paperwork is completed. The exact timeline is spelled out in your settlement agreement and annuity documents.

4. Can I receive structured settlement payments by direct deposit?

Often, yes. Most carriers allow direct deposit to a checking or savings account. If you are currently receiving paper checks and want to switch, contact the insurer or servicing company to request the appropriate forms.

5. Are my structured settlement payments taxable?

For most physical injury or sickness cases, structured settlement payments are tax-free under Section 104(a)(2) of the Internal Revenue Code. However, some types of damages (like punitive damages or certain employment claims) can be treated differently. Always confirm your situation with a tax advisor.

6. Do structured settlement payments increase with inflation?

Most structured settlements are fixed, meaning the payment amounts do not change over time. Some settlements include a cost-of-living adjustment (COLA) clause that increases payments by a small percentage each year, but that must be built into the original design.

7. What should I do if a payment is late or missing?

First, check your bank account and mail for a few days, then contact the customer service department of the life insurance company or administrator listed on your documents. Have your policy or contract number ready. Keep notes of whom you spoke with and what they said.

8. What happens to my structured settlement if I die?

It depends on how your settlement was structured. Some payment streams are “life only” and stop when you die. Others are “period certain” (for example, 20 years certain), meaning payments continue to your designated beneficiary for the rest of the guaranteed period. Your settlement agreement and annuity contract should state which you have.

9. Can I borrow against my structured settlement?

Most life insurers will not let you borrow against a structured settlement annuity directly like a normal life insurance policy. Some third-party finance companies offer loans secured by structured settlement payments, but these arrangements can be expensive and risky. Carefully review terms and seek professional advice before using them.

10. Can I sell my structured settlement payments?

In many jurisdictions, yes—but only after a court reviews and approves the sale under structured settlement protection laws. Selling payments usually means giving up a large portion of their long-term value in exchange for a smaller lump sum today. It is a major decision and should not be taken lightly.

Conclusion: You Now Understand the Payment Engine Behind Your Settlement

Structured settlements can feel mysterious when all you hear is, “Don’t worry, you’ll get payments for life.” But now you know the real answer to how structured settlement payments work:

- The court approves a payment schedule in your settlement agreement.

- The defendant or insurer funds a structured settlement annuity.

- An assignment company and life insurer coordinate to send your payments on time.

With this understanding, you can better protect your documents, monitor your payments, and ask the right questions if anything ever changes. And if you are planning a settlement now, you can work with your attorney or planner to design a payout schedule that truly supports your long-term financial life.

2 thoughts on “How Structured Settlement Payments Actually Work: The 5-Step Path from Court to Your Bank Account”